Welcome to what I hope becomes an annual tradition. I’m a drug developer turned investor focused on private biotech, and these are my predictions for the year ahead

The XBI biotech index surged 37% in 2025, pulling the sector out of its post-pandemic hole. But 2026 will not lift all boats. Four predictions, with a little bonus at the end, capture the year ahead: private capital shifting from caution to calculated risk-taking, China’s emergence as a clinical development hub, acquisition frenzy by patent-imperiled pharma giants, and regulatory chaos that matters less than feared.

1. Giant Series A syndicates crack by year-end

Private biotech will continue to lag the public rebound by 9-12 months. Investors will keep seeking safety in numbers through most of 2026.

Series A rounds offer a useful barometer here because they typically fund companies with something concrete in hand (a development candidate or two approaching the clinic) at prices attractive to both early- and late-stage investors. The 2025 data tells a clear story: investors deployed $8.9B across 108 Series A rounds (a decade low), of which almost 70% were backed by syndicates of five or more investors. That’s not just a decade high—it’s a full doubling from the average of the previous nine years.

This crowding will intensify through mid-2026, creating stark bifurcation. The Haves will secure multi-year runways capable of weathering any storm; the Have-Nots will sprint toward de-risking milestones…or run out of cash.

But here’s where it gets interesting: the biggest outcomes in venture come from betting on underappreciated areas. Toward the end of 2026, expect the first signs of reversal as investors hunt for returns in overlooked opportunities. More total capital will be deployed, spread more evenly across more deals. That means smaller syndicates and lower raise sizes. The megasyndicates will still dominate 2026 headlines, but money will start moving into smaller, higher-reward bets.

2. China starts to import biotech innovation

Everyone knows about the billions of dollars’ worth of assets flowing out of China that dominated 2025, from PD-1/VEGF bispecifics to ADCs. But 2026 will see a quieter revolution: US and EU innovation flowing into China.

EsoBiotec’s $1B acquisition by AstraZeneca in early 2025 proved the model works. The Belgian biotech generated compelling clinical data in China so quickly it leapfrogged more established competitors and got the deal. China thus offers compelling economics, particularly for cell and gene therapies where investigator-initiated trials run by world-class scientists can move fast.

In 2026, more outfits will emerge—from dedicated funds to OTR-style innovative companies—set up specifically to bring US and EU innovation into China, help generate early clinical data quickly, and share in downstream economics through local rights or equity stakes. This won’t be for everyone, and it won’t be without controversy. But the value creation will prove too compelling for the industry to ignore.

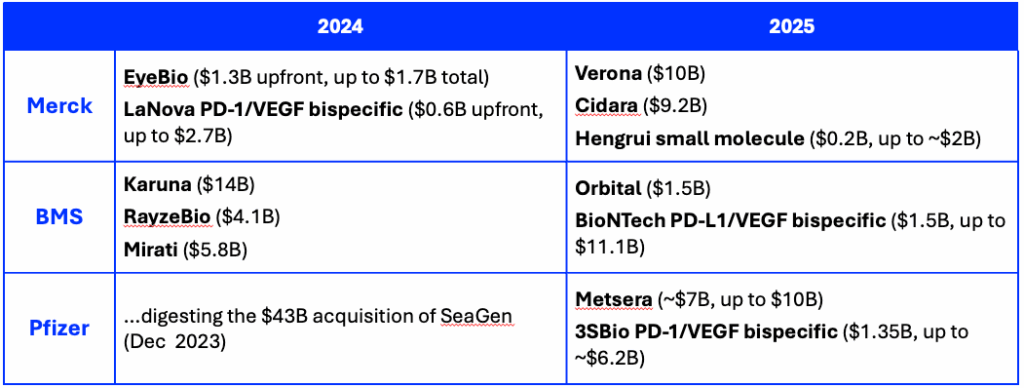

3. Big pharma goes on its biggest M&A spree since 2019

The loss-of-exclusivity cliff everyone’s been dreading? It’s here. Less than three years away and massive.

Merck’s Keytruda is expected to generate roughly $32B in 2025 revenue. Its key competitor, BMS’s Opdivo, brings in around $10B. Both lose critical patent protection in December 2028. Eliquis, the popular anticoagulant worth $13.5B to Pfizer and BMS, starts facing generic competition in April 2028.

Not surprisingly, all three companies have been aggressive buyers. Over just the past two years, they’ve completed multiple billion-dollar-plus transactions:

That’s a lot of capital deployed, but it won’t be nearly enough. Merck especially faces an existential hole when Keytruda revenue evaporates. Reports suggest the company is eyeing Revolution Medicines and its KRAS inhibitor pipeline for around $30B—and that’s probably just the start.

Here’s my call: with biotech survivors from the longest, deepest industry downturn now looking healthier and more affordable than ever, 2026 will be the biggest M&A year since the peak of 2019 when BMS bought Celgene for $74B. The commercial imperative is simply too great, and the targets are finally priced right.

4. Biotechs shrug off regulatory chaos and bet on pragmatic execution

The regulatory landscape has turned chaotic. Biopharma has been running frantic scenario analyses since the Inflation Reduction Act, with its first-ever drug price negotiations, passed in 2022. Then 2025 arrived with FDA and NIH departures, murkier regulatory feedback, curtailed research funding, expanded drug price negotiations, Trump.Rx, supply chain re-shoring mandates, threats of penalties for overseas drug development, and vaccination pullback.

Commercial-stage companies are feeling real pain from these policies and will continue to do so in 2026. But for the vast majority of biotechs, 2026 will be defined by heads-down pragmatism.

Why? Here’s the calculus most pre-commercial biotechs actually face: if you can show your drug works for $5M instead of $10M, do it in 12 months instead of 24, and avoid regulatory delays or uncertainty in the process, you take that deal. Especially when your drug has an 80%+ probability of clinical failure anyway and the hypothetical regulatory penalties are years away on a commercial product that probably won’t exist. The bite from these regulatory headlines is simply too far down the line to matter for most biotechs’ immediate decisions.

Commercial-stage companies face different math. They’re dealing with supply chain mandates and working through FDA uncertainty, which could dampen their M&A appetite. But most have already negotiated their Most Favored Nation price agreements, and their patent cliffs still need plugging.

Bottom line: 2026 will be steady as she goes. Volatility, whiplash headlines, but most biotechs will keep their heads down and execute.

5. Bonus

As a former drug developer, I’d be remiss if I didn’t highlight a few programs worth watching in 2026. All are in public biotech pipelines; all could deliver outsized patient benefit. And since I invest only in private companies, I have no financial stake in any of them. In no particular order:

Revolution Medicine’s RMC-5217 targets the G12V mutation of KRAS, long considered undruggable. It’s not the company’s lead program, but Merck’s rumored interest suggests they got something right.

DiaMedica’s DM199 is a recombinant protein with $5B potential in stroke. It’s a sleeper that investors will start paying attention to once interim data drops in the second half of 2026.

Xenon’s XEN1701 is a small molecule inhibitor targeting Nav1.7, which has a strong genetic validation for pain treatment. The Phase 2 proof-of-concept study starts in 2026.

Oral obesity drugs – too many to list. Novo’s and Lilly’s price concessions on their obesity blockbusters completely changed the landscape in 2025 by making combinations reimbursable. Small molecule obesity drugs, less effective than traditional peptides, will now be able to reach comparable efficacy when combined. With the efficacy barrier gone, their low manufacturing costs will drive market share and determine winners.

The Bottom Line

2026 is not a year for biotech tourists. The tide is turning, but the currents remain treacherous. My bet is on disciplined spending paired with clear-eyed, pragmatic execution. Success will require both, plus deft navigation of geopolitical headwinds.

I’m looking forward to grading myself on these next year. In the meantime, I’d love to hear what you think I’m getting wrong (or right).